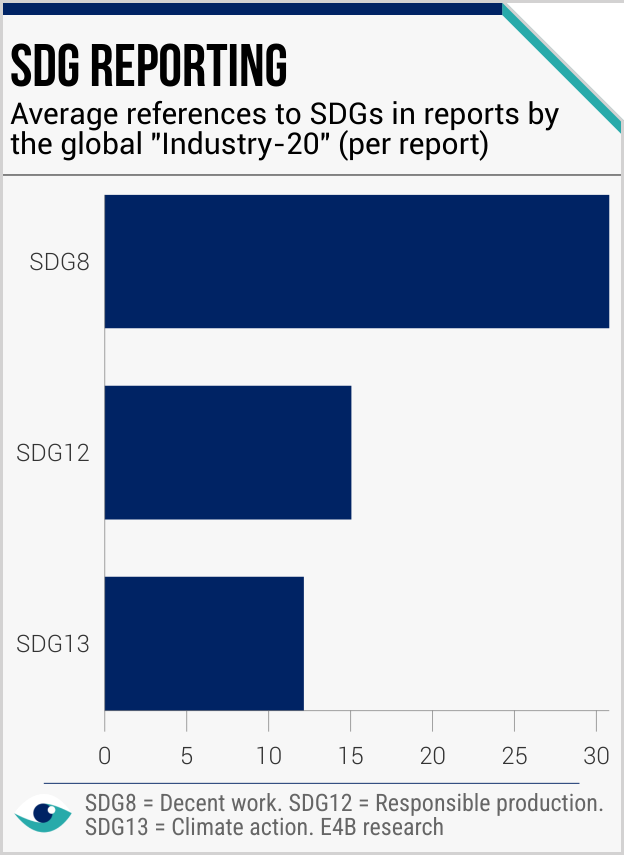

Corporate sustainability reporting has become essential, yet many companies face challenges aligning their operations with the SDGs. Increasingly, firms focus on SDG8 (Decent work), SDG 12 (Responsible production) or SDG13 (Climate action), though many fail to demonstrate clear links between actions and goals. Despite the rise in corporate sustainability reporting, many disclosures focus solely on positive impacts, leaving significant gaps in transparency. To address this, firms must balance reporting by including both successes and challenges, set measurable goals linked to the SDGs and advocate for more meaningful and actionable reporting standards.

Global focus

The measure of a business: SDG impact and transparency

Reporting entities should consider balanced SDG-related disclosures, reflecting positive impacts and challenges, to ensure accountability

UN Sustainable Development Goals

Global (all industries)

AT A GLANCE

Many companies fail to provide balanced SDG disclosures, positively screening impacts and omitting challenges.

This imbalance undermines stakeholder trust and prevents a full understanding of corporate sustainability efforts, especially in high-impact areas like SDG8, SDG12 and SDG13.

Inadequate SDG reporting can damage corporate accountability and hinder SDG progress.

Positive bias in SDG reporting

Many companies limit SDG disclosures to highlight only positive impacts. This approach results in skewed reporting that overlooks the challenges and risks faced. Such practices contribute to the impression that firms are managing their image rather than delivering tangible progress. Selective reporting or SDG-washing erodes credibility and hinders stakeholder engagement.

Voluntary SDG frameworks

Frameworks like the UNGC and SDG Compass guide corporate sustainability efforts, but their voluntary nature limits their effectiveness. Studies have shown that firms using these frameworks still make incomplete disclosures, particularly in areas where performance lags. This selective use of voluntary frameworks creates gaps in reporting. Without regulation and improved scrutiny, the credibility of SDG reporting is unlikely to improve.

Gaps in Global North coverage

There are significant gaps in SDG reporting across regions, with large firms active in developing countries and high-polluting industries generally more engaged in SDG reporting compared to those in developed countries. This disparity raises concerns about coverage in certain regions and sectors. Additionally, small firms and those in emerging markets often lack comprehensive reporting frameworks.

Trends among leading firms

Among the cohort of 20 leading reporting entities globally we analyse (the “Global Industry-20”), it is perhaps not a surprise that all entities disclose some degree of commitment or action to SDG8 (Decent work), SDG 12 (Responsible production) or SDG13 (Climate action). However, the majority of these disclosures reflect only general commitment to the SDGs and fairly weak causal links between entity-level actions and the overall goals. This in part reflects the nature of the SDGs as overarching policy ambitions more appropriate for country-level planning, implementation and accountability. Nevertheless, there is also an aspect of SDG-related corporate disclosure that must urgently be improved if it is to resonate with stakeholders as an indicator of sustainability performance.

FURTHER READING

- SDG Compass (GRI, UN Global Compact and WBCSD)

- Corporate reporting on the SDGs (Journal of Accounting and Organizational Change - 2024)

- SDGs in corporate responsibility reporting (Journal of Management and Governance - 2024)